How Does Section 174 Affect How We Capitalize Software Development Costs?

Written by

Status

answered

Written by

Status

answered

Section 174 used to feel like a finance problem. Engineering teams wrote software, tracked payroll, and shipped features, while finance handled the tax treatment later.

That became more difficult once software development costs had to be examined more closely. The question was no longer just how much the company spent on engineering. It became a matter of what kind of engineering work was done, where it was performed, and whether the records could support the tax treatment used.

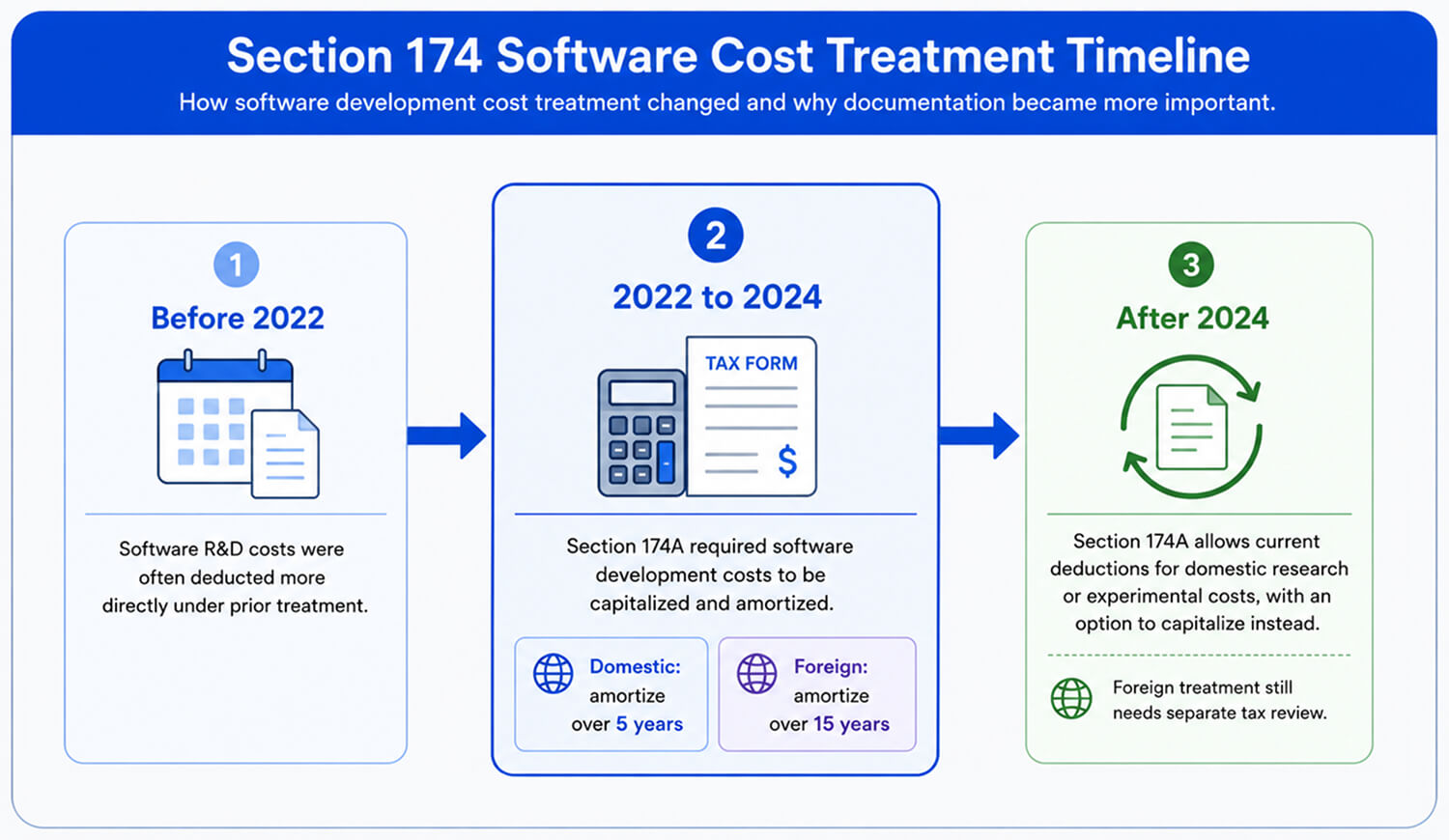

For tax years beginning after December 31, 2021, Section 174 required specified research and experimental expenses to be capitalized and amortized, including software development. Domestic costs were generally amortized over five years, while foreign costs were amortized over 15 years.

The recent law added Section 174A, which allows current deductions for domestic research or experimental expenditures for tax years beginning after December 31, 2024, and provides an election to capitalize and amortize those domestic costs instead. Foreign treatment still requires separate review with tax advisors.

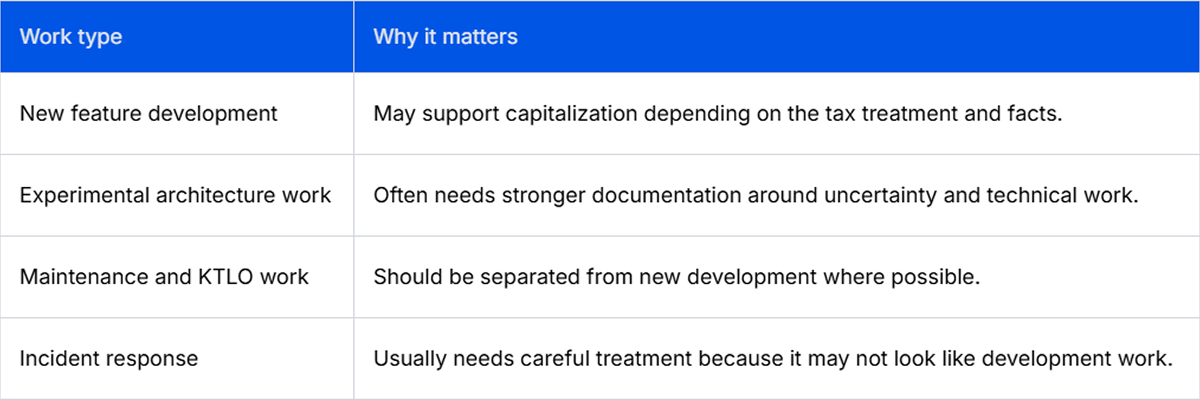

For engineering leaders, the practical issue is not the code itself, but classification. A sprint may include new product work, bug fixes, infrastructure cleanup, security remediation, customer support work, and internal tooling. Some of that may relate to R&D capitalization or software capitalization. Some of it may not.

This caught teams off guard because engineering systems were not designed to capture tax evidence. Jira, GitHub, CI logs, incident tickets, and planning docs describe delivery work, but they often do not clearly identify cost categories. A ticket labeled “API cleanup” may involve experimental architecture work, routine refactoring, or maintenance. The label alone is weak evidence.

Software development costs are not uniform from a financial perspective. A developer may spend Monday designing a new search ranking service, Tuesday fixing flaky tests, Wednesday reviewing pull requests, and Thursday responding to a production incident. Payroll sees one person. Engineering sees normal work. Tax teams need a supported allocation.

This is also why KTLO engineering maintenance should not be hidden within broad product buckets. Keeping the lights on is real engineering work, but it should not be blindly mixed with new software investment.

Useful documentation is usually already close to the work. Teams do not need a separate tax journal for each developer. They need a better structure for the records they already create.

A practical evidence trail usually includes:

The weak version of this is a spreadsheet built once a year from memory. The stronger version is a lightweight process in which projects, work types, and effort allocation are captured as work is underway.

Engineering managers can help without slowing teams down. Project tags should be clear. Epics should state the business and technical purpose. Pull requests should link back to the work item. Design docs should explain why the work was needed, not just what changed.

Finance needs sufficient detail to apply Section 174 and related rules. Engineering needs to protect the delivery flow. Both sides lose when the process becomes a quarterly archaeological exercise.

The cleanest setup is usually a shared operating model. Finance defines the cost categories and evidence requirements. Engineering identifies where that information can be captured with the least friction. When teams also use GenAI tools in development, Milestone can help measure adoption, ROI, workflow visibility, and engineering performance alongside routine project and cost reviews.

This work also fits naturally into engineering budget planning. If leaders already review how engineering time is allocated, they can use that same visibility to support tax and capitalization discussions. The goal is not to make developers think in tax language. The goal is to make engineering work visible enough that finance does not have to rely on assumptions.

A monthly review is usually better than a year-end scramble. Review large projects, mixed work streams, offshore development, internal tools, platform work, and major refactors. These are the areas where classification questions tend to arise.

Section 174 made software capitalization harder to ignore. Even with newer domestic deduction rules under Section 174A, engineering teams still need cleaner records of software development costs. Good documentation does not need to be heavy. It needs to be consistent, close to the work, and clear enough for finance to trust.